A $10,000 annual SaaS invoice paid by card can burn almost $300 in fees. The same payment through stripe ach fees using ACH Direct Debit may cost only $5.

That gap gets attention fast. Still, finance teams know the sticker price is only half the story, because timing, returns, and reconciliation shape the real cost of online payments. Here's the practical view, based on Stripe's current pricing as of March 2026.

Current Stripe ACH Direct Debit pricing in March 2026

As of March 2026, Stripe's ACH (automated clearing house) Direct Debit pricing shows 0.8% processing fee, capped at $5. Stripe has kept that rate steady into 2026, but pricing can change over time, so it's smart to recheck before you update models or customer billing rules.

The core formula is simple: transaction fee = min(payment amount × 0.008, $5).

That means the cap kicks in at $625. Below that point, the fee scales with the payment. Above it, the fee stops growing.

Here's what that looks like in practice:

| Payment amount | ACH fee | Effective rate |

|---|---|---|

| $100 | $0.80 | 0.80% |

| $625 | $5.00 | 0.80% |

| $1,000 | $5.00 | 0.50% |

| $8,000 | $5.00 | 0.06% |

The big takeaway is simple: on larger invoices, the effective rate drops fast.

Stripe also applies related ACH costs that finance teams should track in reporting. A failed ACH Direct Debit costs a $4 transaction fee. A disputed ACH payment costs a $15 dispute fee. Stripe's separate ACH Credit product is priced differently, at $1 per payment, so don't mix those numbers into your Direct Debit analysis.

Above $625, the fee stops climbing. That breakpoint matters more than the 0.8% headline.

There's no monthly fee tied to standard ACH Direct Debit pricing in the current Stripe materials. For implementation details, mandate authorization, and bank account collection flows for recurring payments, Stripe's ACH Direct Debit documentation is the best technical reference.

When ACH beats cards on SaaS margins

For SaaS teams, ACH usually wins hardest on high-ACV invoices and predictable renewals. That's where the $5 cap changes the math.

To see the spread, compare ACH with Stripe's common credit card fees of 2.9% + 30¢:

| Payment amount | ACH Direct Debit | Domestic card | Fee savings with ACH |

|---|---|---|---|

| $100 | $0.80 | $3.20 | $2.40 |

| $1,000 | $5.00 | $29.30 | $24.30 |

| $10,000 | $5.00 | $290.30 | $285.30 |

Because of that gap, ACH fits well for annual upfront contracts, enterprise renewals (more efficient than wire transfers for high-volume recurring payments), usage true-ups, and invoice-driven collections. In those cases, even a modest shift from cards to ACH can move gross margin in a visible way.

Still, cheaper doesn't always mean better for every flow. Self-serve monthly plans often convert better on cards via stripe checkout, because customers trust them and activation feels instant. ACH can add bank account verification friction, and payment confirmation is delayed. Stripe's Financial Connections facilitates Instant Bank Payments to help reduce some of that friction. So while ACH is still cheaper on a $49 subscription, the savings may not beat the conversion hit.

That's why many SaaS teams use a split approach across payment methods. They keep cards for low-touch signup and push ACH for larger invoices, contract renewals, or accounts with a known billing contact as the optimal payment method. Stripe's ACH debit overview lines up with that pattern, especially for recurring or invoice-based payments tied to US bank accounts.

Timing, returns, and reconciliation matter more than the sticker price

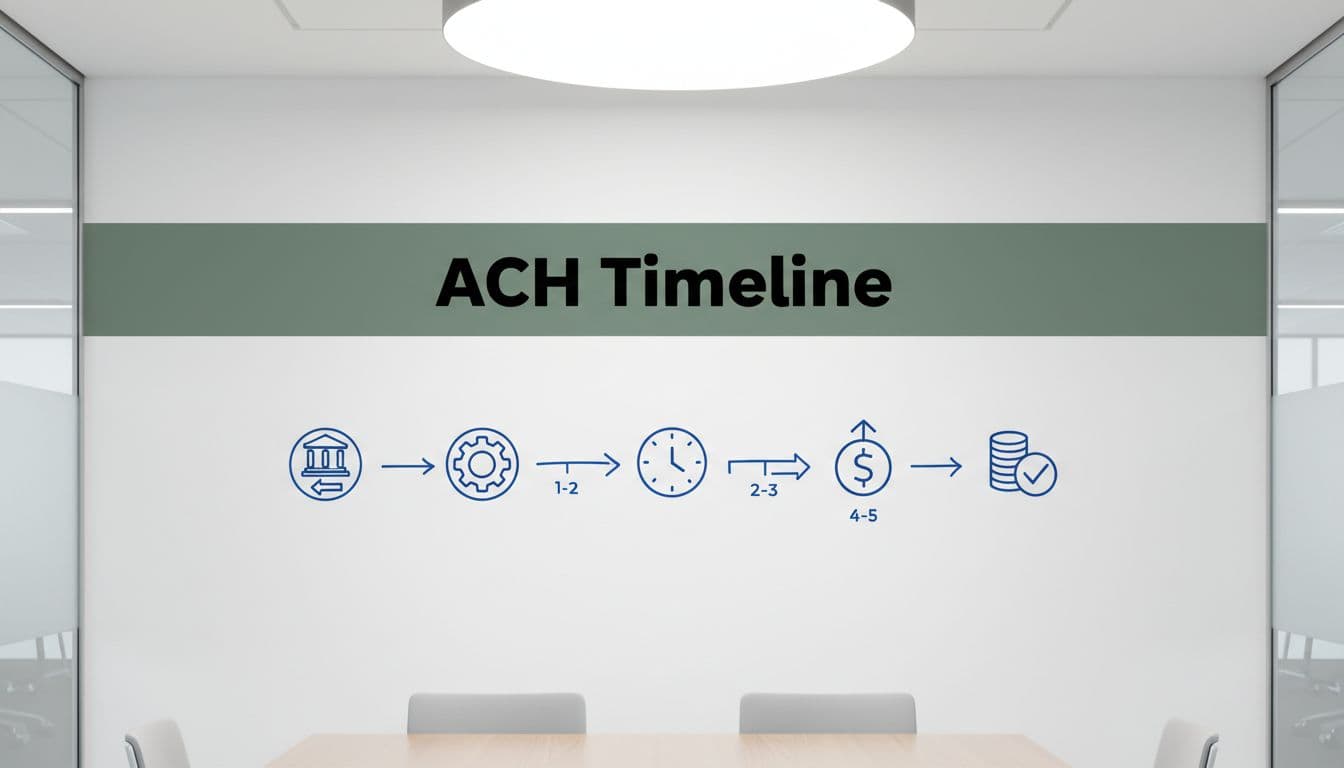

ACH is cheaper because it's a slower rail. Settlement timing matters, with standard settlement taking about 4 business days on Stripe, while eligible users may access faster settlement in about 2 business days. At the same time, the bank can still reject the debit after submission, so treasury timing matters.

Think of cards as a toll road and ACH as freight rail. Freight is cheaper, but it doesn't arrive the same day.

That difference affects close processes, dunning, and revenue operations. If your team marks an invoice as fully safe the moment ACH is initiated, you can create bad reporting and awkward customer follow-up later. Stripe also notes that customers can dispute ACH debits well after payment, often up to 60 days in unauthorized cases.

A few operating rules make ACH work better:

- Separate initiated from settled cash: Post the payment event, but don't treat it like final cash until the risk window is clear after 4 business days or faster settlement.

- Watch failure patterns: Each failed ACH debit costs $4 in transaction fees, so weak bank data hygiene can eat into savings. Issues like insufficient funds are common, but using microdeposits twice or direct verification with the routing number improves bank account verification hygiene. Check patterns in the Stripe dashboard.

- Handle returns fast: Use return reasons to drive retry rules, customer outreach, and account holds. Stripe's ACH returns guide is useful here, especially to avoid refund fees; monitor via the Stripe dashboard and Stripe Connect for platforms.

- Match billing motion to payment rail: ACH is best when invoice value is high enough that the savings beat the extra waiting and support work. Tools like Stripe Terminal can help manage payment methods alongside ACH Direct Debit.

There are also 2026 setup details to keep on the radar. Stripe has moved ACH toward newer payment flows like the payment intent API and mandate authorization, and newer Nacha rules add classification requirements for some goods-related transactions. For most pure software subscriptions, that won't change pricing, but it does make clean setup more important, including strong routing number checks and microdeposits for bank account verification.

ACH looks cheap on the fee line. It stays cheap only when your return rate and posting rules stay tight.

The strongest takeaway is simple: stripe ach fees are excellent for larger SaaS payments, because the $5 cap changes unit economics fast compared to credit card fees. But the real win comes only when your team accounts for slower settlement, failed debits, and return handling across payment methods.

Review your payment mix by invoice size and billing motion. If big renewals still default to cards or wire transfers, that's usually the first margin fix worth making. Optimize your payment method with Stripe Checkout for online payments, switching more volume to ACH over other payment methods for better online payments economics.