A small payment fee can eat into SaaS margin faster than most teams expect. That is especially true when recurring bills are large, predictable, and tied to Australian bank accounts.

Stripe BECS fees are worth a close look in 2026 because they can cut payment costs on local subscriptions without changing your product or pricing model. The cap matters, the timing matters, and the real savings show up when you compare them with card and wallet payments across your customer mix.

What Stripe BECS fees look like in 2026

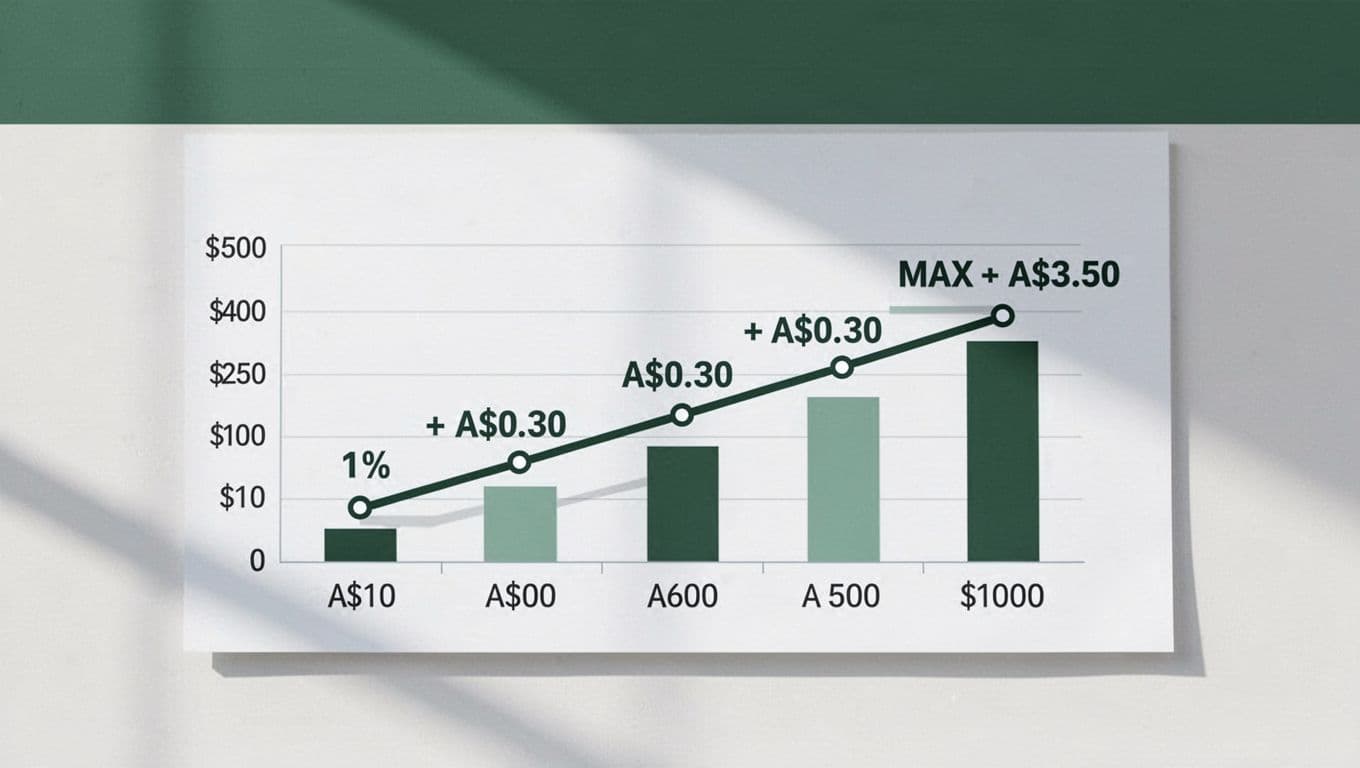

As of May 2026, Stripe lists Australia BECS Direct Debit at 1% of the transaction amount plus A$0.30, with a maximum fee of A$3.50 per payment. That cap is the part most SaaS owners care about. A larger invoice does not keep getting more expensive forever.

For recurring billing, this gives you a cleaner cost line than cards in many cases. It also fits subscription-style payments well, because the customer authorizes bank debits once and Stripe keeps the billing flow moving after that. Stripe's subscription setup guide for BECS Direct Debit shows how recurring billing works in Australia.

There is a tradeoff. BECS payments take a few business days to settle, so cash does not hit instantly. Stripe's BECS processing times guide explains the timing in more detail. For SaaS, that delay is often acceptable if the savings are real.

Why the cap matters more for SaaS

For SaaS, the fee story is rarely about one transaction. It is about hundreds or thousands of renewals that repeat every month. That is why small differences in rate turn into real SaaS payment processing costs over a year.

The cap changes the math on higher-value plans. A customer paying A$50 a month barely moves the needle. A customer paying A$500 or A$1,000 a month is different. At that point, the flat cap starts doing the heavy lifting.

Once invoices rise above a few hundred dollars, the cap matters more than the headline percentage.

That is also why monthly, annual, and usage-based billing behave differently. Annual plans may create larger single charges, which makes BECS more attractive. Smaller monthly plans may still benefit, but the savings are less dramatic.

If you want a tighter view of where the money leaks, detailed Stripe fee diagnostics for SaaS help separate BECS from cards, FX, and dispute costs. A blended average often hides the real story.

A simple Stripe fee breakdown for common subscription sizes

This part is easier to see in numbers. The math below uses Stripe's current BECS formula and the A$3.50 cap.

| Subscription amount | Stripe BECS fee | Effective fee rate |

|---|---|---|

| A$50 | A$0.80 | 1.6% |

| A$100 | A$1.30 | 1.3% |

| A$500 | A$3.50 | 0.7% |

| A$1,000 | A$3.50 | 0.35% |

The pattern is simple. The fee rate drops as the invoice grows, until the cap takes over. That is why BECS can be a strong fit for SaaS plans with mid-market and higher-value Australian customers.

It also helps to check the payment mix, not just the total. A company with 80% local renewals and 20% cross-border card volume will not have the same effective rate as a company that sells mostly overseas.

Stripe vs PayPal fees for Australian SaaS

When people compare Stripe vs PayPal fees, they often focus on the visible rate and stop there. That misses the bigger picture. PayPal usually sits much higher on Australian commercial transactions, while BECS stays lower for local bank debits.

For a quick example, a A$100 BECS payment costs A$1.30 before any other business-level costs. A similar PayPal commercial payment can land much higher. Over a year of renewals, that gap adds up fast.

| Payment method | Fee on A$100 | Fee on A$1,000 |

|---|---|---|

| Stripe BECS | A$1.30 | A$3.50 |

| PayPal commercial fee | A$3.70 | A$34.30 |

That gap is why many SaaS teams route local Australian customers toward bank debit when the billing setup allows it. Cards still matter, especially for international customers and one-off checkouts, but BECS can be the cheaper rail for recurring domestic revenue.

For a broader market view, this Stripe vs PayPal comparison for Australia is a useful reference point. It helps frame where wallet payments fit, and where bank debit is the better cost choice.

How to reduce Stripe fees without hurting subscriptions

If you want to know how to reduce Stripe fees, start with payment selection, not pricing hacks. The cheapest fix is usually to send the right customer to the right payment method.

A few moves usually matter most:

- Route Australian recurring customers to BECS when they have an eligible bank account. This keeps the lowest-cost method in front of the people who can use it.

- Watch invoice size. Larger subscriptions benefit more from the BECS cap, so segment high-value plans carefully.

- Reduce failed-payment retries. Every failed attempt adds friction and can create extra payment work, even when the base fee looks small.

- Separate local and cross-border revenue. FX and international charges can erase the savings you get from a lower domestic rate.

A Stripe fee calculator is useful for a first pass, but it rarely tells the full story. It may show the fee on a clean transaction, yet skip the costs tied to retries, disputes, FX, and mixed payment methods. Those details matter more in SaaS than in one-off commerce.

If your billing stack is growing, how FeeTrace analyzes Stripe transactions is a practical place to see how the full fee picture gets built from actual transaction data. That matters because the effective rate is what hits margin, not the advertised rate.

Track the real fee rate, not the headline rate

The best SaaS teams treat payment fees like a living metric. They do not check once a year and move on. They watch the mix of payment methods, customer locations, and invoice sizes because those inputs change the bill.

That is where FeeTrace pricing by Stripe volume can help if you want to see whether fee analysis pays for itself. The point is not to add another dashboard. The point is to find the transactions that cost too much and fix the ones that matter most.

If you want a fast way to review your own setup, Analyze My Fees gives you a direct starting point. It is most useful when you already know Stripe is a major cost line and you want to see where BECS, cards, FX, and failed payments are hitting you.

Conclusion

Stripe BECS is one of the cleaner ways to cut payment costs for Australian SaaS in 2026. The combination of a percentage fee and a hard cap gives you better control as invoice values rise.

The real win comes when you compare payment methods across your customer base, not just the published rate. If your local recurring revenue is large enough, Stripe BECS fees can lower your effective rate in a way cards and wallets often cannot.

What matters most is the full picture, not the single number on the pricing page.