Stripe refund fees can wipe out more margin than they seem. Even after a refund is issued, the customer often gets the full payment back, while your original processing fee stays gone.

That gap looks small on one invoice. Across monthly plans, annual prepaids, and promo-heavy launches, it adds up fast. Finance teams should regularly check the Stripe Dashboard to analyze how these costs impact net margins. If you run finance, RevOps, or billing, you need clear rules for cash, revenue, and reporting.

How Stripe refund fees usually work in 2026

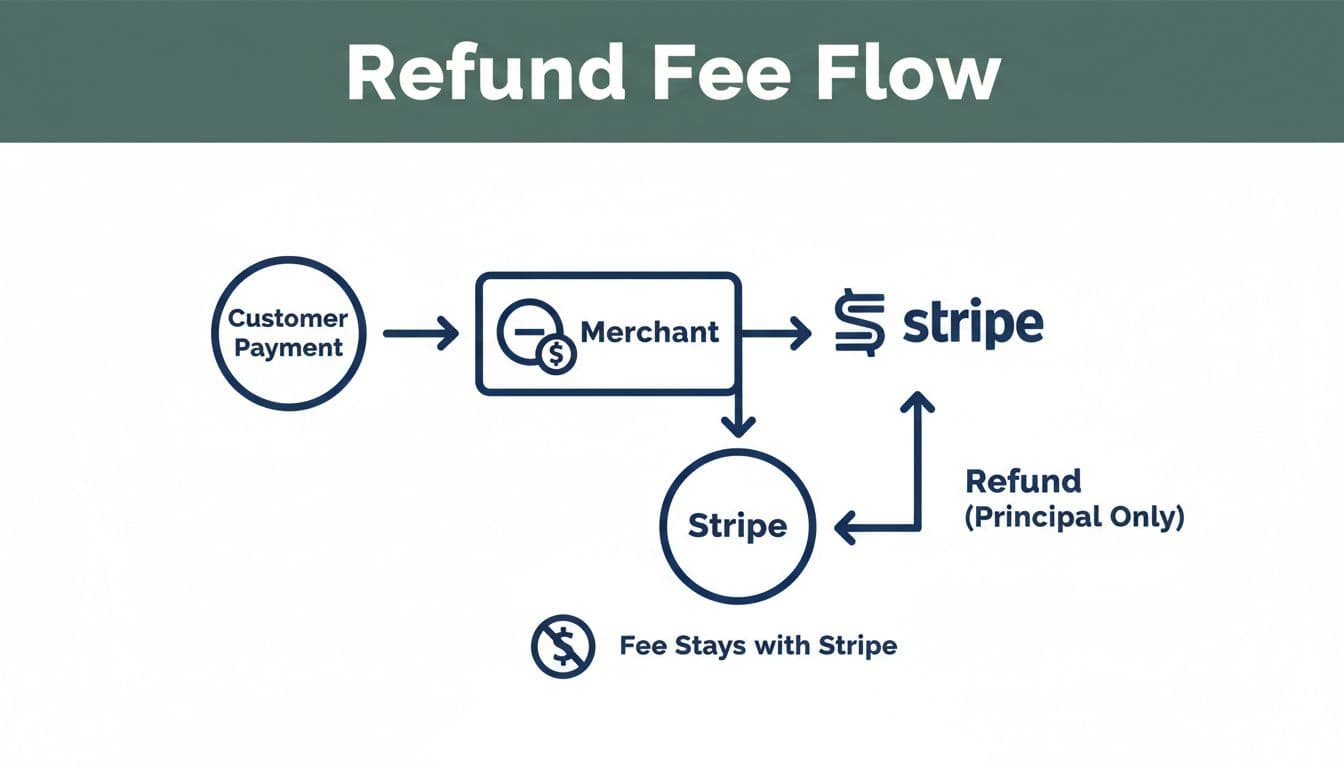

As of March 2026, Stripe's standard rule is simple. Once a successful transaction occurs, Stripe usually returns the customer's transaction amount, but it does not return non-refundable fees like the original processing fee.

For a common US card example, a $100 charge at 2.9% + 30¢ leaves you with $96.80. If you later issue a full refund, the customer gets $100 back, and the original processing fee of $3.20 remains your cost. A partial refund works the same way. Stripe does not hand back part of that processing fee.

Still, don't treat one example as universal. Stripe pricing and fee treatment can vary by country, payment methods, contract, and volume tier. US domestic cards may differ from international cards or those involving currency conversion, where the original processing fee changes. Different payment methods, such as bank-based options, can also follow varying refund rules.

That's why finance teams should confirm both Stripe's refund documentation and its support page on refunded payment fees before they build forecasts or internal policy.

Another detail matters at close. Refunds come out of your available Stripe balance. If the balance is short, Stripe may hold a card refund as pending until funds land. So the approval date and the cash date may not match. The refund process usually takes 5 to 10 business days before appearing on a bank statement. A card issuer might request an Acquirer Reference Number for tracking, with technical considerations like failed refunds or manual authorization.

For SaaS teams, that means return policy belongs in both customer support playbooks and finance controls as the baseline for these actions using various payment methods. The customer sees a charge reversal. Your P&L still carries the processing fee loss.

What refunds do to cash, net revenue, MRR, and ARR

Refunds impact financial reporting beyond simple support actions. They alter cash flow, gross-to-net revenue, and recurring metrics, so integrate them properly into your accounting software for accurate tracking.

This simple table shows the math on a $100 subscription charge at standard US card pricing, using the Stripe Dashboard as the authoritative source for these metrics:

| Scenario | Cash after original processing fee | Cash after refund activity | Processing fee recovered? | Reporting impact |

|---|---|---|---|---|

| No refund | $96.80 | $96.80 | No issue | Normal revenue and MRR |

| Full refund of $100 transaction amount | $96.80 | -$3.20 net | No | Reverse revenue, remove related MRR/ARR |

| Partial refund of $20 transaction amount | $96.80 | $76.80 | No | Reduce revenue by refunded amount |

The pattern is clear. Revenue can reverse fully or partly, but the original processing fee usually stays lost as non-refundable fees.

Here's the common SaaS mistake: teams reverse the cash correctly, yet leave the metric story messy. If a new customer buys a $100 monthly plan and gets a full refund three days later, most finance teams should not leave that customer sitting in new MRR. If the sale fed ARR, that ARR usually needs to come back out too.

On the other hand, not every refund changes MRR. If you refund a one-time onboarding fee, usage overage, or setup charge, you may reduce revenue without changing subscription MRR at all. Similarly, a mid-cycle partial refund may reflect a service issue, not churn.

Because definitions vary, align the treatment with your internal metric policy and board pack logic. This isn't legal or tax advice, and revenue recognition rules can differ by business model, timing, and jurisdiction. Still, the operating lesson is simple: book the refund, book the retained processing fee, and keep your MRR and ARR rules consistent.

Refunds, disputes, credits, and the metrics to watch

Refunds, chargebacks, and customer credits are three different events. If your team mixes them together, margin analysis gets muddy fast.

A refund is voluntary. Your team approves it in Stripe as part of the refund process. A dispute or chargeback starts with the customer's bank, contrasting sharply with voluntary refunds. That usually costs more, because you can lose the sale, lose the original processing fee, and face a dispute fee as well. Current Stripe programs often involve a fee around $15, but that can vary by country, currency, program, and contract. Tools like Stripe Radar serve as a critical tool for mitigating these chargeback risks.

For platform-based businesses using Stripe Connect, these distinctions matter even more. A customer credit is different again. No cash leaves today. Instead, you reduce a future invoice or create account credit. For a SaaS company, that can be the better fix when the customer stays active and you want to avoid a full cash refund.

Treat refunds, disputes, and credits as separate buckets, or your true payment cost will look better than it is.

Finance teams should review refund rate every month using the Stripe Dashboard, not only total refund dollars. Track both refund count and refunded amount as a share of successful payments in your financial reporting. Then break that data by plan, market, acquisition source, and time-to-refund. Fast refunds often point to billing confusion. Slower refunds can signal support, product, or fit problems.

External refund rate analysis also shows why this matters. Refund spikes can become early warning signs for dispute growth and payment risk.

The best teams don't stop at totals. They trace refunds back to root causes, audit their return policy to reduce friction, then fix billing copy, invoice timing, plan packaging, and handoffs before disputes rise. Streamlining the refund process early helps prevent escalation.

A single refund fee can look harmless. Across a quarter, it becomes a quiet margin leak.

Start with your last 90 days of refunds. Verify your Stripe terms using the Stripe Dashboard, separate refunds from disputes and credits, and tighten the reporting rules around stripe refund fees and the associated processing fee before small losses turn into a pattern.